This article was originally published two months ago on Fundflicks only. However, about 3 weeks ago they decided to halt articles contribution from independent writers, so I am now able to share this article here.

Before sharing the article, I would like to highlight its recent Q3 performance. Its another strong set of quarterly numbers from the group with revenue up by 28% and EPS up by 46%.

The momentum is definitely strong and they now guided a year-on-year revenue growth of 33%. Last quarter, the guide was in excess of 30% and it was 26% in Q1.

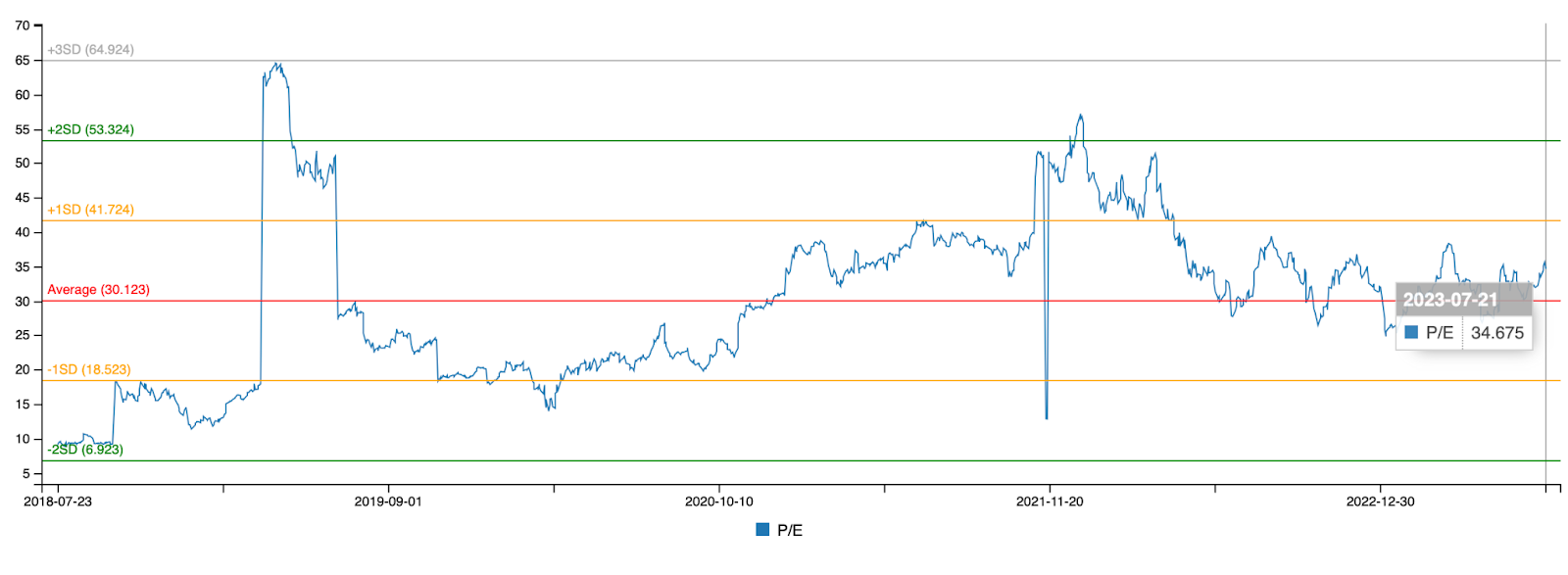

The price has appreciated a whopping 74% year to date. Despite that gain, its forward PE is still at a reasonable 32x. Just a little higher than their average PE over the past 5 years of 30x.

As written in my article below, growth does not come linearly for ANET, so do expect softness in their numbers during certain quarters or year, but over a longer time frame, the company has shown that they can grow at an annual rate of above 20%.

While ANET is already a 3-bagger for me, I am not selling yet as I believe it still has a long growth path ahead.

Original article written on 26 July 2023 and updated on 2 August 2023

Which companies come to your mind when you hear chatGPT and metaverse?

Yes, I am sure you will think of the two titans Microsoft and Meta which at the time of writing have a market cap of US$2.8B and US$0.81B! Both are fantastic companies that penetrate our daily lives. However, today I am not going to write about them but a company who has partnered both of them in the backend, Arista Networks (ANET)

Overview

Arista Networks describes itself as an industry leader in data-driven, client to cloud networking for large data center, campus and routing environments.

It is not easy to understand what the above really means unless you are in the industry. I struggle with it too but the thing is we do not have to fully understand a company before making an investment. True to be told, most of us would not understand the nitty gritty of the various businesses that we invest in.

Having said that, it is good to have a rough idea about the nature of its business. In short, Arista Networks is in the business of providing high speed network switches for businesses that require a network. Cisco (CSCO) is the well-known name in the sector but ANET has been taking market share from it since it was founded in 2008. Primarily, they disrupted the network space with their cloud networking solutions.

If you would like to know more about the company, you can watch the following YouTube video. You can also find out more information on their IR website.

Finally, being recognised in research from both Gartner and Forrester shows how well placed the company is in the industry.

Leadership

“Level 5 leadership is a concept developed in the book Good to Great. Level 5 leaders display a powerful mixture of personal humility and indomitable will. They’re incredibly ambitious, but their ambition is first and foremost for the cause, for the organization and its purpose, not themselves.”

https://www.jimcollins.com/concepts/level-five-leadership.html

It’s hard to judge the leaders and culture unless one works at the organization. However, a quick check on Glassdoor shows a good rating on the company with a high approval of the CEO. The most common comment I saw was “working with smart and intelligent people”.

It does seem to me that the ANET’s leaders are at or close to Level 5. At the very least, they are founder-leaders. Two of the founders Andy Bechtolsheim and Kenneth Duda are still there and CEO Jayshree V. Ullal has been the CEO since 2008. The other key management such as COO Anshul Sadana and CFO Ita Brennan have been with the team for many years.

In terms of shareholdings, Andy and Jayshree own 14.9% and 3.3% of the company. So they are definitely aligned to the performance of the company.

Crunching the numbers

ANET is definitely growing over the past 5 years but as seen from the numbers, the growth can be uneven. This is something that one has to accept when investing in the company. The company’s growth is dependent on the customers’ spending which is based on their business cycle. As such, there will be moments when the customers will hold back their spending.

The impact is felt more when the decision comes from META or MSFT as both are still contributing significantly to ANET’s revenue. A search on the net shows META contributed 25.5% and MSFT contributed 16% to ANET’s revenue in the last financial year. While I do not disagree that this is a risk, it can be perceived as a moat too. With the strong relationship built over the years, the likelihood of META and MSFT ditching ANET as their partner is low.

As such, the best way to judge its performance is to measure its compound annual growth rate over a 5-year period. For the past 5 years, ANET has grown its top line and bottom line by a good 21% and 26% annually. ANET has also been free cash flow positive and in a net cash position over the past 5 years. This augurs well for the company as it continues to grow with its customers.

At the time of writing, it is trading at a PE of 34, which is just slightly higher than its average of 30. If ANET can repeat its 5-year EPS growth rate of 26%, then the current PEG ratio will be 1.3x which is really quite reasonable, given the huge total addressable market.

Latest Results and Future Prospects

In 2023Q1, ANET has produced an outstanding performance with revenue and EPS up by a whooping 54% and 61% respectively. However, the growth should be more muted in the coming quarters, given that they endorsed a 26% growth in revenue for the full financial year.

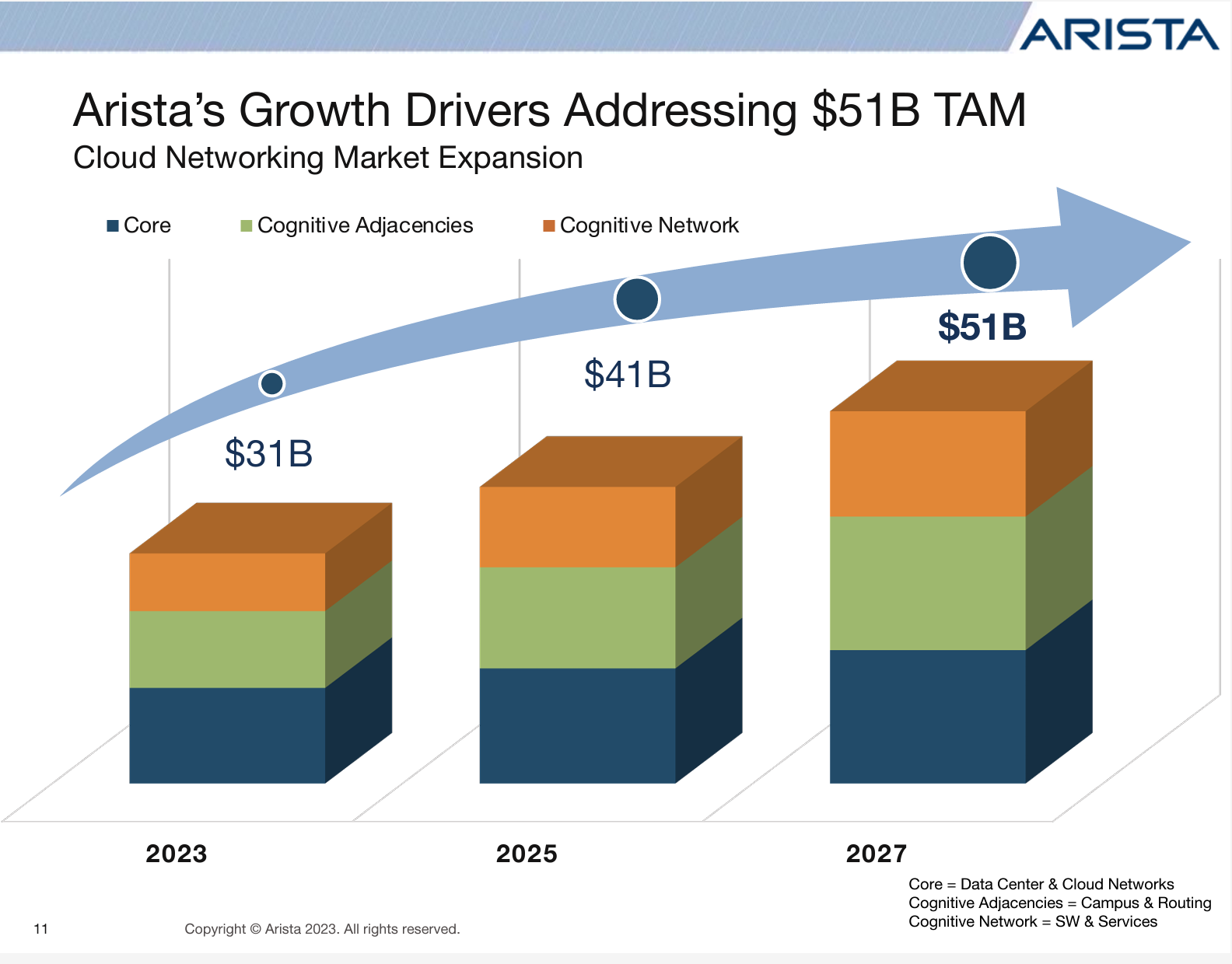

Looking further, ANET has projected a total addressable market of $51b by 2027. With the current year’s revenue to come in at around $5.5b, they have much room to grow into.

Conclusion

Arista Networks is not an easy company to understand as its business is highly technical. The good thing is as investors, we do need to fully understand the business. As long as the management is able to grow the business, then it can form part of our investment portfolio.

Given how ANET has disrupted the incumbent and continues to capture market share over the past decade, it has earned itself a strong reputation. With this track record, I am assured that they are not a fluke and have the capacity for further growth.

While ANET has tried to diversify from its two major customers META and MSFT, they still contribute to a high percentage of their revenue currently. So the performance of these two customers would have an impact on ANET and that might result in lumpy growth.

With the development of AI and metaverse in the coming decade, the demand for network power and speed will only increase and ANET is set to benefit from this trend and continue to grow at least at a reasonable rate.

Latest update (2 August 2023)

Arista delivered another outstanding quarter that exceeded expectations. Revenue increased by 39% and EPS up by 46%. Yes, the growth is less than Q1 but is much higher than expected. Also, with greater visibility, they are now guiding a year-over-year growth in excess of 30% instead of the 26% guidance given in Q1.

The graph below shows the updated financial information.

We can see why the growth for next two quarters, especially Q4 will be much more muted. They are up against very strong numbers in Q3 and Q4 2022 as there was a ramp up by the cloud titans.

The price has jumped after the earnings release. It closed at a price of $185.61 at the end of today, 19.7% higher than yesterday’s price. That value is at a forward PE of about 31 which again is very reasonable for a leader in a growing industry.